Legal Notice:

Please read the website Terms and Conditions, Privacy Policy and Disclaimer before proceeding. These contain important legal and regulatory disclosure and information relevant to this website. This website uses cookies to enhance user experience and track usage statistics.

By continuing to use this website you:

• Confirm that you have read, understand and agree with the website Terms and Conditions, Privacy Policy and Disclaimer.

• Agree that you are a Professional Client or Eligible Counterparty as described in the disclaimer and you acknowledge that this website is not intended for Retail Clients. If you are in doubt as to what type of customer you are you should consult your financial adviser.

Investors willing to take advantage of volatility can capitalise on the long-term outperformance of small-cap stocks – and now could be a great time to do just that.

Elephants don’t gallop, is a phrase coined by legendary British small-cap investor Jim Slater.

As the saying suggests, we instinctively know that smaller, more agile companies can perform better than their larger, more cumbersome counterparts over the long term.

Yet all too often, investors are misled by the higher levels of volatility exhibited by small-cap stocks. And ironically, as you will learn from this article, it is during these times of higher volatility that the best buying opportunities for small caps arise.

For those willing to participate in the small-cap market and take advantage of the volatility, the long-term rewards can be highly lucrative. But the best returns come when utilising the right kind of fund manager.

In this article we’ll explain why now is a great time to start investing in the small-cap market, with small caps having been sold off relative to their larger peers. You’ll also learn which kinds of managers to avoid, and which ones have the greatest potential to outperform in a major way.

Small is beautiful. Since 1927, US small caps have outperformed US large caps by around two percentage points on an annualised basis. This “small-cap premium” phenomenon was first highlighted by Eugene Fama and Kenneth French in their Fama/French stock pricing model in the 1990s. The rationale behind this model is that smaller companies are riskier and less liquid than their larger counterparts. To compensate for their greater risk, they need to offer investors an excess return.

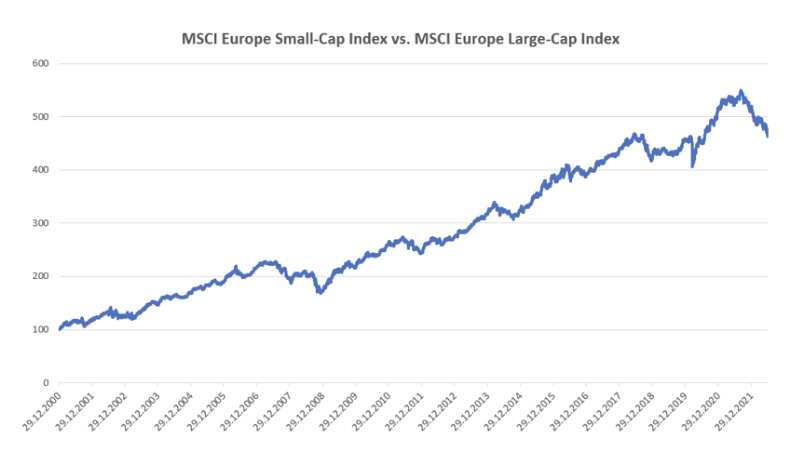

This is a feature of small caps in general, rather than just a US phenomenon. As can be seen from the following chart, European small cap companies have also produced significant outperformance since the turn of the millennium.

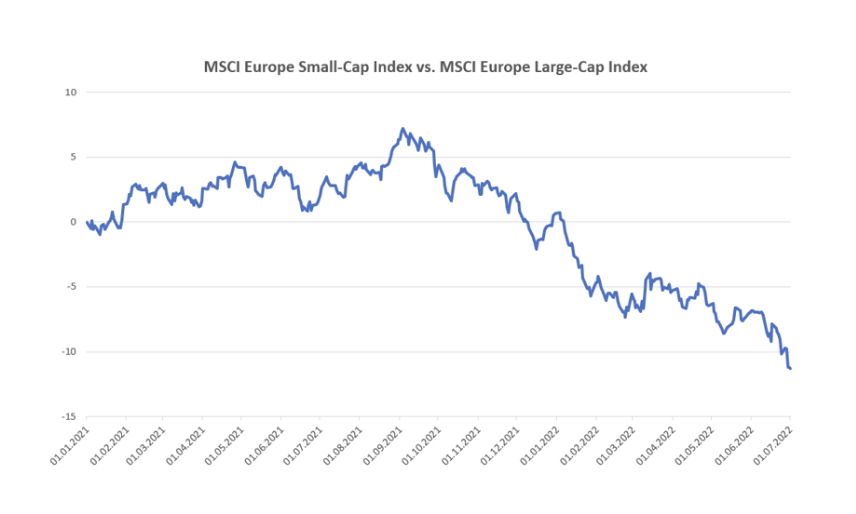

This long-term outperformance comes at the cost of occasional periods of under-performance. As can be seen from the next chart, the past year has been one such period of significant underperformance for small-cap stocks.

So why are small caps out of favour right now?

The first point is that smaller companies are more sensitive to economic cycles as they are more reliant on GDP expansion than their larger counterparts. Given that the outlook for economic growth has soured of late, investors have naturally shifted their attention towards their larger, less risky counterparts.

Also, smaller companies are more exposed to rising prices as they tend to be price takers rather than price setters. As inflation has accelerated, some smaller companies will have seen their profit margins eroded by higher input costs which they may have struggled to pass on to their customers.

Central banks are now taking action to tighten monetary policy in order to bring inflation under control. In the US there are some tentative signs that inflation is beginning to roll over and the expectation is that inflation will begin to trend lower over the coming months, especially as lower oil prices begin to take effect.

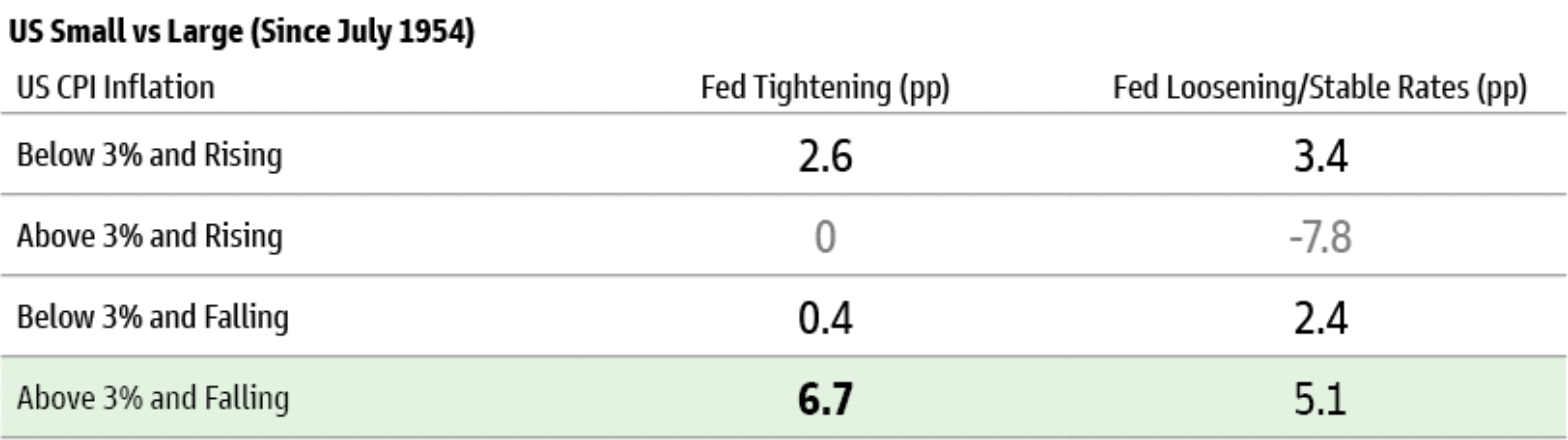

History shows that small caps tend to outperform when inflation falls from a high level, even when monetary conditions are being tightened (see chart below).

While recession risk is certainly a concern for small caps, the market appears to have priced this into valuations to some extent. What’s more, small caps tend to outperform in the years following a recession, primarily due to their greater levels of domestic exposure and higher levels of operational gearing. In the three years following the dot-com crash, for example, small caps outperformed large caps by 42%. A similar pattern played out in the three years following the 2008 great financial crisis, when small caps outperformed large caps by 32%.

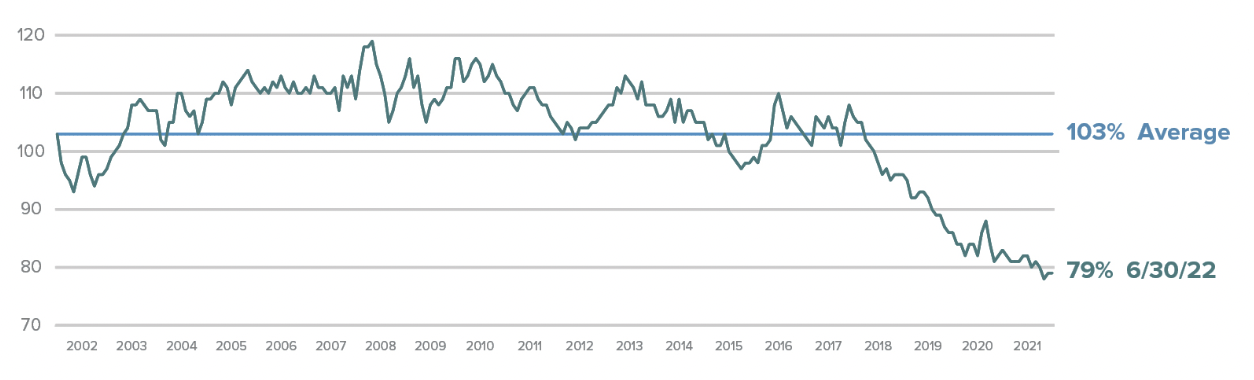

With the mood music currently of the sombre variety, small cap stocks are currently trading at the most attractive levels in decades (see chart below).

Russell 2000 vs. Russell 1000 Median LTM EV/EBIT (ex. Negative EBIT Companies) From 6/30/02 to 6/30/22

In contrast to the 3% premium that small caps have historically commanded over their larger counterparts, they are currently trading at a 20% discount. This may be justified if the current slowdown does prove to be a severe recession, but anything short of that and the current divergence could prove to be a fantastic buying opportunity.

Unless you are comfortable (and have the time for) picking and managing small-cap stocks yourself, you are going to need a fund manager to do it for you. Naturally, your first port of call might be your financial adviser, who will probably point you towards a small-cap fund from one of the large investment houses. However, these products rarely offer the best in terms of performance potential.

Fund products from larger investment outfits tend to get recommended to clients by advisers because they pay larger commission and don’t represent any career risk to the adviser (nobody ever got the sack for underperforming conventionally). While these fund products will provide you with exposure to the small-cap sector, the trouble is they rarely feature in the top of the league tables because they are provided by organisations that are focused on asset gathering, which often makes the fund less nimble than smaller counterparts.

But who are these smaller counterparts? These are the boutique owner-managed funds where the manager has typically left employment in the large institutions in favour of going it alone. The fact that only the best managers would consider setting up their own funds is one factor that sorts the wheat from the chaff, but there is data to back up the superior returns on offer from boutique managers.

According to a 2018 study conducted by US-based Affiliated Managers Group (AMG), boutique active investment managers have outperformed both non-boutique peers and indices over the last 20 years.

The chart below shows the average annual outperformance of boutiques versus non-boutiques:

As you can see, boutiques did best in US small-cap value equity, outperforming non-boutiques by 1.62 percentage points per year. This is unsurprising, as the small-cap markets offer the best opportunity for boutique managers to gain an edge on their larger counterparts, as smaller companies are often less well researched.

But the very best returns came from picking the right boutique managers to invest with, according to AMG, whose study showed that top decile and top quartile boutiques outperformed by 2.76 percent and 1.71 percent, respectively.

Research suggests that new fund managers tend to produce the best returns in the early years of their existence, which probably has a lot to do with the fact that they are focused primarily on portfolio management rather than AuM growth. Once their attention turns to the latter their returns often suffer as a result.

When you’re looking for a small-cap manager make sure you ask them how big they plan to grow their AuM. Is there a cap on AuM which would lead to a soft close? Can they continue to operate with an edge as their AuM grows? Will they have to become less concentrated over time? Does the manager have skin in the game? These are the factors that will determine whether the manager can maintain their track record over time.

Picking the right manager should help ensure you can capitalise on the long-term outperformance potential that small caps can bring to your portfolio.

Disclaimer: This blog is intended for informational purposes only. This blog is not intended to invite, induce or encourage any persons to engage in any investment activities and is not a solicitation or an offer to buy or sell any stock, investment product or other financial instruments. If in doubt, please seek financial advice from an independent financial adviser. Sarnia Asset Management is licensed by the Guernsey Financial Services Commission (GFSC). Past performance is not an indication of future returns. Investments carry risk, including the risk that you will not recover the sum that you invested.

By James Faulkner

Oops! You are using an outdated browser!

Click here to upgrade your browser in order to view this page.